Paid preparers of federal income tax returns or claims for refund involving the Earned Income Credit (EIC) must not only ask all the questions required on Form 8867, but must meet the due diligence requirements in determining the taxpayer’s eligibility for, and the amount of, the EIC. Those who prepare returns claiming EIC must meet due diligence requirements in four areas:

- Completion and submission of Form 8867

- Computation of Credit

- Knowledge

- Retention of Records

Preparers who fail to meet the due diligence requirements can be assessed a penalty of $530 for each failure to meet all four due diligence requirements for each EIC claim. See I.R.C. §6695(g) and Part VI of Form 8867.

Completion and Submission of Form 8867

The purpose of Form 8867 is to ensure that the tax preparer has considered all applicable EIC eligibility requirements for each prepared tax return. You should ask questions applicable to each client and be able to explain the meaning and reasoning behind each question. Form 8867 should be completed based on information provided by the taxpayer to the tax return preparer.

- Complete Form 8867, Paid Preparer’s Earned Income Credit Checklist, to make sure you consider all EIC eligibility criteria for each return prepared.

- Complete checklist based on information provided by your client(s).

- For returns or claims for refund filed electronically, Form 8867 will be submitted with the return.

- For returns or claims for refund not filed electronically, attach the completed form to any paper return you prepare and file.

- For returns or claims for refund you prepare but do not submit directly to the IRS, provide completed Form 8867 to the taxpayer to send with the filed tax return or claim for refund.

Computation of Credit

Keystone Tax Solutions Pro calculates the correct amount of Earned Income Credit on the tax returns that you prepare. Special rules regarding the treatment of income, deductions, credits, etc. in certain circumstances are all taken into consideration. The calculation is based strictly on the information and data that is entered into the tax return, and it is the responsibility of the taxpayer to ensure the accuracy of all figures used in the calculation of the EIC.

Complete EIC worksheet from the Form 1040 instructions, or Publication 596, Earned Income Credit, or a document with the same information. The worksheet shows what is included in the computation, that is, self-employment income, total earned income, investment income, and adjusted gross income.

Knowledge

The knowledge requirement states you must not know, or have reason to know, that any information used in determining your client’s eligibility for, or the amount of, EIC is incorrect. How to comply with the knowledge requirement:

- Know the law and use your knowledge of the law to ensure you are asking your client the right questions to get all relevant facts.

- Take into account what your client says and what you know about your client.

- Make additional inquiries if the information is incomplete, inconsistent, or incorrect, as a reasonable and well-informed preparer would determine.

- Document at the time of the interview any additional questions you ask and your client’s answer.

The Treasury Regulations give examples of the application of the knowledge requirement. Find current regulations for tax return preparer due diligence requirements here and proposed regulations here.

Retention of Records

The IRS requirement for keeping records may be more extensive than you realize. Use the following list as a guideline to ensure you are retaining copies of all IRS required documentation.

- Keep a copy of the Form 8867 and EIC worksheet, and a record of any additional questions you asked your client to comply with your due diligence requirements, along with your client’s answers to those questions.

- Keep copies of any documents your client gives you that you use to determine eligibility for, or the amount of, the EIC.

- Verify the identity of the person giving you the return information and keep a record of who provided the information and when you got it.

- Keep your records in either paper or electronic format, but make sure you can produce them if the IRS asks for them.

- Keep these records for 3 years from the latest date of the following that apply:

- The original due date of the tax return (not including any extension of time for filing), or

- If you electronically file the return or claim for refund and sign it as the return preparer, the date the tax return or claim for refund is filed, or

- If the return or claim for refund is not filed electronically and you sign it as the return preparer, the date you present the tax return or claim for refund to your client for signature; or

- If you prepare part of the return or claim for refund and another preparer completes and signs the return or claim for refund, you must keep the part of the return you were responsible to complete for 3 years from the date you submit it to the signing tax return preparer.

EIC Due Diligence Warnings

To assist you with ensuring compliance, you may see Due Diligence Warnings like this:

The first warning indicates that not all the Due Diligence questions have been answered. The second warning indicates that there are no notes entered in the return. Notes are desirable and in the case of an audit may prove invaluable to you.

To satisfy the Due Diligence Warnings, from the Main Menu of the Tax Return (Form 1040), select:

- Payments, Estimates, EIC

- Earned Income Credit

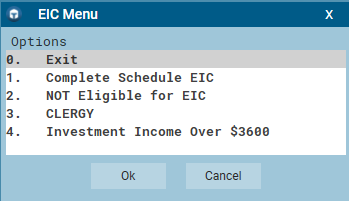

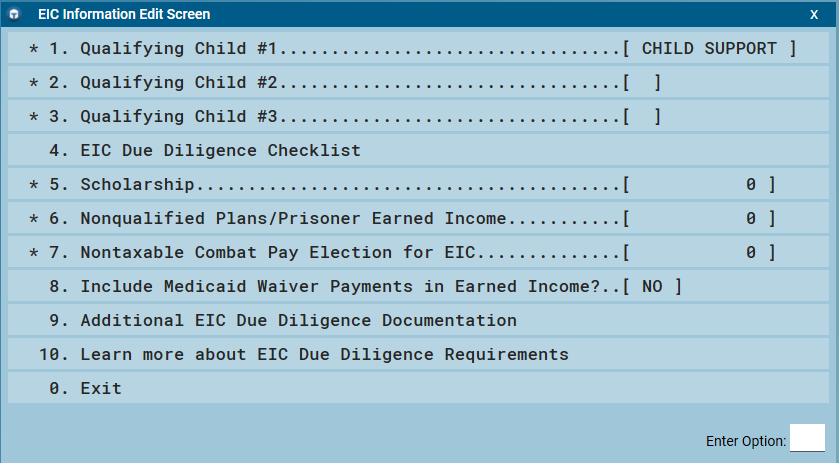

Select Complete Schedule EIC. If the return contains qualifying children, select EIC Due Diligence Checklist:

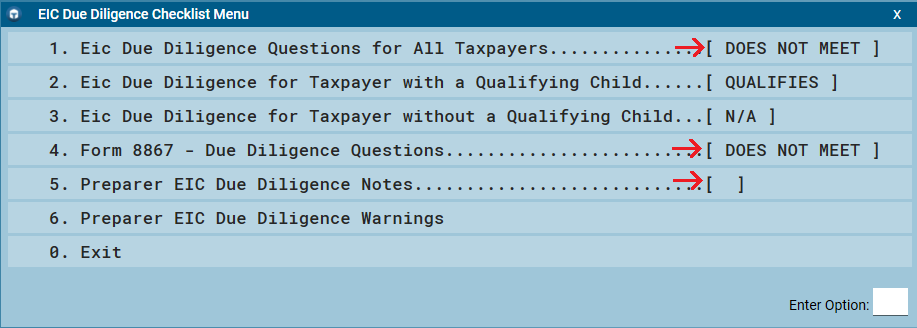

In the EIC Due Diligence Checklist Menu, look for any lines that indicate something needing completion as indicated by “DOES NOT MEET”:

Enter notes in Preparer EIC Due Diligence Notes.

Even after completing your due diligence requirements, a return may not qualify to receive EIC. There is a report available in the return to help diagnose why. To see the report, from the Main Menu of the Tax Return (Form 1040) select

- View Results

- Why No EIC Calculated

Note: This article is a discussion of the due diligence requirements pertaining to the Earned Income Credit and how to record due diligence in the Keystone Tax Solutions Pro Program. It is not intended as tax advice. The preparer is strongly encouraged to review the underlying resources linked in the article and referenced in Additional Information below and .

Additional Information